When your doctor prescribes a brand-name medication and your insurance says no, it’s not just a paperwork hiccup-it’s a health crisis waiting to happen. You’re not alone. In 2022, nearly 18% of prior authorization requests for specialty drugs were denied, and over 60% of those were for brand-name medications. The reason? Insurers often say there’s a cheaper generic alternative. But what if that generic doesn’t work for you? What if switching causes seizures, severe side effects, or hospital visits? That’s where the appeal process becomes your lifeline.

Why Your Insurance Denied Your Brand-Name Medication

Insurance companies don’t deny brand-name drugs because they’re cruel. They do it because they’re bound by formularies-lists of approved drugs they’ll pay for. These lists are designed to cut costs. If a generic version exists, insurers will push it first, even if your body has already proven it doesn’t respond to it. You might get denied because:- The drug isn’t on their formulary anymore

- They require you to try a cheaper drug first (step therapy)

- They say there’s no proof the brand-name is medically necessary

- Your doctor didn’t fill out the prior authorization form correctly

What You Need Before You Appeal

You can’t appeal blindly. You need evidence. And the most powerful evidence comes from your doctor. Start by requesting your Explanation of Benefits (EOB) from your insurer. It’s required by law to be sent within five business days of the denial. Read it carefully. It will tell you the exact reason for denial-like “generic alternative available” or “no prior authorization submitted.” Write that reason down. Next, call your doctor’s office. Don’t email. Call. Ask for a letter of medical necessity. This isn’t just a note. It’s a detailed clinical argument. A good letter includes:- Your diagnosis and how the medication treats it

- Specific failures with generic alternatives (e.g., “Patient experienced three episodes of uncontrolled seizures after switching to generic levetiracetam”)

- Lab results, hospital records, or previous treatment history

- How the brand-name drug improves your quality of life

- The exact drug name, dosage, and prescribing doctor’s NPI number

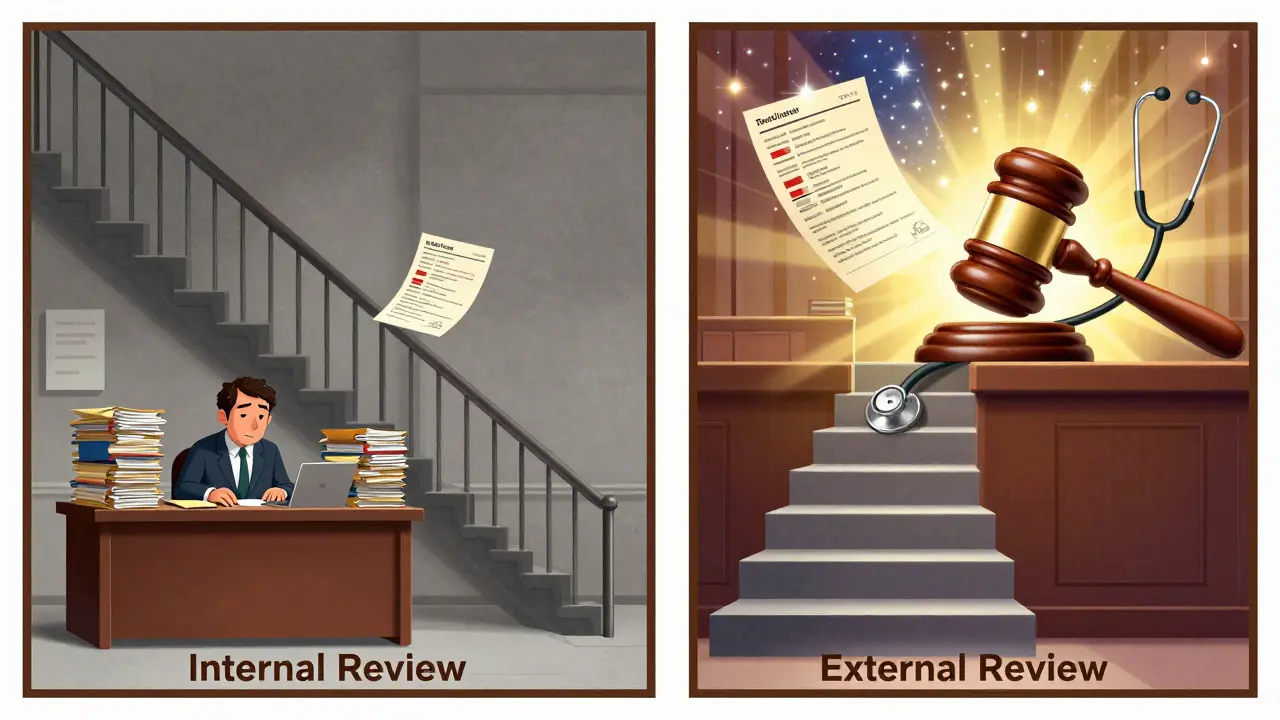

The Two-Stage Appeal Process

There are two official steps: internal appeal and external review. Stage 1: Internal AppealThis is your first shot. You submit your letter, EOB, and any supporting records directly to your insurer. You have up to 180 days to file (120 days for Medicare). For urgent cases-like insulin, seizure meds, or cancer drugs-you can request an expedited review. Insurers must respond in 4 business days. Don’t just mail it in. Call every few days. Kantor & Kantor’s data shows appeals with daily follow-up calls are processed 28% faster. Keep a log: who you spoke to, when, what they said. If they say “we’re reviewing,” ask for a case number. Write it down. Stage 2: External Review

If your internal appeal is denied, you can request an external review. This is where things change. Instead of an insurance employee deciding, an independent third party reviews your case. Success rates jump here. CMS data shows 58% of external reviews approve coverage for brand-name drugs-nearly double the internal appeal rate. For urgent cases like insulin, approval rates hit 72%. Who handles this? It depends on your plan:

- If your insurance is through your employer (ERISA plan), contact the U.S. Department of Health and Human Services

- If it’s a state-regulated plan (like Medicaid or individual marketplace), contact your state’s insurance commissioner

Why Most People Fail-And How to Avoid It

The biggest mistake? Waiting too long. A 2022 Patient Advocate Foundation survey found that 61% of people felt overwhelmed. Many waited months before acting. By then, they ran out of medication, missed work, or ended up in the ER. Another common error: sending a generic letter. “My patient needs this drug” isn’t enough. You need specifics. “Patient developed severe hypoglycemia on generic insulin, requiring three emergency room visits in six months” is what wins. Also, don’t try to do it alone. If your plan is governed by ERISA (which covers 61% of Americans), legal help increases your success rate by 47%. That doesn’t mean you need a lawsuit. It means hiring an attorney who specializes in insurance denials to draft your appeal. Many offer free consultations. Some even work on contingency.What to Do While You Wait

Appeals take time. But you can’t stop taking your medication. Many drug manufacturers offer patient assistance programs. Eli Lilly’s Insulin Value Program, for example, gives eligible patients brand-name insulin for $35 a month while their appeal is pending. Other companies like Novo Nordisk and Sanofi have similar programs. Check their websites or call their patient support lines. Some pharmacies offer bridge programs-short-term supplies while you wait. Ask your pharmacist. They often know about local options. And if you’re in a crisis? Go to your doctor. They can write a letter requesting a temporary override. Some insurers will approve a 30-day supply while your appeal is processed.

What’s Changing in 2026

The system is slowly getting better. The 2023 Consolidated Appropriations Act now requires Medicare Part D plans to show real-time coverage info before you even fill a prescription. That means fewer surprises. New federal rules also require insurers to track how long they take to approve or deny requests. If they’re slow, they get penalized. The Biden administration’s 2023 Executive Order pushed CMS to enforce these rules harder. Still, the system is broken. Doctors spend over 13 hours a week just managing prior authorizations. Insurers approved 22% more brand-name medication requests in 2023 than in 2022-meaning they’re denying more, not fewer. The future? AI will help. Some insurers are testing automated systems that flag truly necessary prescriptions before they’re denied. Experts predict this could reduce inappropriate denials by 30-40% in the next five years. But right now? Your best tool is persistence. Documentation. And your doctor’s voice.What to Do If Your Appeal Is Still Denied

If you’ve done everything-letter, follow-ups, external review-and you’re still denied, you have options:- Request a formal written denial letter with the exact legal basis

- File a complaint with your state’s attorney general’s office

- Seek help from a patient advocacy group like the Patient Advocate Foundation

- If you’re on an ERISA plan, consult an attorney about federal litigation (though this is expensive and complex)

Final Checklist: Your Appeal Survival Kit

Before you start, make sure you have:- Copy of the denial letter (EOB)

- Letter of medical necessity from your doctor (with specific clinical details)

- Your insurance policy number and member ID

- Prescription details: drug name, dose, frequency

- History of failed generic trials (lab results, ER visits, doctor notes)

- Case number and contact info for your insurer’s appeals department

- Calendar reminder to follow up every 3-5 days

What if my doctor won’t write a letter of medical necessity?

Ask to speak with the office manager or practice administrator. Many clinics now have standardized templates for these letters. If they still refuse, request a copy of your medical records and bring them to a different provider-like a specialist or urgent care-who can review your case and write the letter. Some patient advocacy groups can also connect you with doctors who specialize in writing these appeals.

How long do I have to appeal after a denial?

You have up to 180 days for most private insurance plans under federal law. Medicare gives you 120 days. Medicaid timelines vary by state-check your state’s health department website. For urgent cases, you can request an expedited review, which must be decided within 4 business days. Don’t wait. The sooner you start, the better your chances.

Can I get my medication while my appeal is pending?

Yes. Many drug manufacturers offer patient assistance programs that provide free or low-cost medication during appeals. Eli Lilly, Novo Nordisk, and Sanofi all have programs for insulin and other specialty drugs. Your pharmacist may also offer a short-term bridge supply. Call your insurer and ask if they’ll approve a temporary 30-day supply while your appeal is reviewed.

Why do insurers deny brand-name drugs when generics are available?

Insurers prioritize cost over clinical need. Generics are cheaper, so they’re placed on preferred tiers. But generics aren’t always interchangeable. Some patients have allergies, absorption issues, or unpredictable reactions. Insurers often ignore this because their systems are built around cost savings, not individual health outcomes. That’s why your doctor’s detailed letter is critical-it forces them to look beyond the price tag.

Is it worth hiring a lawyer to appeal?

If your plan is governed by ERISA (which covers most employer-based insurance), yes. Kantor & Kantor’s data shows appeals drafted by attorneys have a 47% higher success rate. Insurance companies use legal teams to deny claims, and they know how to exploit loopholes. A lawyer doesn’t mean a lawsuit-they help you write a legally sound appeal that meets federal standards. Many offer free consultations and only charge if you win.

What’s the difference between internal and external review?

Internal review is handled by your insurance company’s own staff. External review is done by an independent third party-like a medical board or state agency. Success rates are much higher in external review: 58% compared to 39% for internal appeals. External reviewers don’t work for the insurer, so they’re less biased. Always pursue external review if your internal appeal is denied.

asa MNG

January 24, 2026 AT 18:06Dolores Rider

January 25, 2026 AT 20:20John McGuirk

January 25, 2026 AT 21:07Michael Camilleri

January 27, 2026 AT 12:49Darren Links

January 29, 2026 AT 00:19Kevin Waters

January 30, 2026 AT 07:33Don Foster

January 30, 2026 AT 07:36siva lingam

January 30, 2026 AT 16:44Himanshu Singh

January 31, 2026 AT 00:14Elizabeth Cannon

January 31, 2026 AT 06:27Patrick Gornik

January 31, 2026 AT 19:40